Lab Grown Diamond Industry Trends 2026: The Smile Curve Reshaping

Lab Grown Diamond Industry Trends 2026: The Smile Curve Reshaping

The lab grown diamond industry trends in 2026 reveal a classic “smile curve” structure: high profits at both upstream equipment/rough production and downstream brand retail, with midstream cutting squeezed in the middle. However, the lab-grown diamond supply chain is undergoing a profound restructuring.

The core paradox of the market can be summarized in one sentence: “World-leading capacity, collapsing profits, and an urgent search for a new anchor.”

Upstream: Rough Stone Production and Equipment—The Ups and Downs of the “World’s Factory”

Reality 1: China Controls 80%+ Global Capacity, with Henan Leading the Way

The lifeline of the global industry is held in Henan (Zhecheng, Zhengzhou, and Nanyang). The top four producers—Zhongnan Diamond (Sinofit), Huanghe Whirlwind, Vigorous New Materials (Power Diamond), and Huifeng Diamond—consume over 80% of China’s gem-grade rough capacity.

Reality 2: Clear Division Between Two Technical Routes

- HPHT (High Pressure High Temperature): Monopolized by China, with over 90% of global capacity in Henan. The cubic press is a proprietary weapon, producing 3-6 carat rough diamonds per 36-48 hour cycle, dropping cash costs to $200-$250/ct.

- CVD (Chemical Vapor Deposition): Previously dominated by the US, Europe, and India, Chinese players like Sifangda (with its 2-million-carat Zhengzhou mega-factory), Worldia, and Carbon Six Technology are catching up, focusing on large sizes and high-purity industrial thermal heat sinks.

Reality 3: Collapsing Gross Margins

During the 2020-2021 peak, upstream gross margins hit 60-70%. By H1 2025, Vigorous New Materials saw its lab-grown diamond gross margin plummet by 78% year-on-year.

Sinofit accumulated nearly 2.9 billion RMB in inventory, pushing the industry sales-to-production ratio down to 12-13%—a textbook case of oversupply. Export prices to India dropped to $8.7/ct, shifting rough diamonds toward an “industrial commodity” pricing logic.

Future Shifts

By 2026, homogenous capacity expansion for gems has paused. Top players are shifting flexibly between gem-grade and industrial diamond slicing. The true capital story lies in diamond heat sinks for AI server cooling (with thermal conductivity 5.6 times that of copper).

Furthermore, top-tier large stones (3ct+, D/IF) still command premiums, locking rough prices to “volume growth with price stability.”

Midstream: Cutting and Processing—The Weakest Link Seeking Backshoring

Reality 1: Indian Dominance

Surat, India, accounts for approximately 80–90% of the world’s cutting and polishing volume, while China accounts for only about 3%. The pattern is a classic one: “Raw stones produced in China → Cut in India → Sold worldwide.”

Reality 2: Low Value-Add Trap

Midstream cutting yields net margins of only 6-8%. In FY2026, India’s lab-grown export volume rose 30.6%, but export value dropped 10.4%, reflecting an intense midstream price war.

Reality 3: It’s not that China can’t produce cutting and grinding tools; rather, it faces a shortage of skilled workers and high labor costs.

In the past, the numbers didn’t add up, so they preferred to sell rough diamonds to India at a low price, have them processed there, and then buy the finished diamonds back.

Future Shifts

Zhengzhou is closing this gap. Through the Henan Lab-Grown Diamond Promotion Center, the region is building smart cutting lines to bring high-value processing (large carats, fancy cuts, colored diamonds) back to China.

Furthermore, AI-assisted cutting is a major variable, utilizing computer vision for flaw identification to reduce waste and challenge India’s labor-cost advantage.

A dominant “China produces, India processes, and the U.S. consumes” triangle has taken shape

In the short term, the “China-India-U.S.” division of labor (production-processing-consumption) will remain unchanged, but China will gradually capture the high-margin segment for itself

Downstream: Brands and Retail—The Most Profitable Frontier Lacking a “De Beers”

Situation 1: China only sells materials; it doesn’t build brands.

The gross margin at the retail end of the value chain can reach 60–70%, representing the other end of the “smile curve,” but this is contingent on your ability to establish a brand premium rather than simply selling loose stones.

Situation 2: A Significant Gap in Market Penetration Between China and the U.S.

Lab-grown diamonds account for approximately 61–70% of engagement rings in the United States, compared to only about 30% in China, indicating that the domestic market is still in its early stages of development. Given the current era of information equality, China’s market penetration rate should catch up quickly.

Situation 3: The channel landscape is highly fragmented.

Shuibei in Shenzhen, China, is effectively the country’s wholesale hub, where large volumes of cultured diamond solitaire rings—priced from a few hundred to several thousand yuan—are sold primarily online, as they are virtually impossible to move in brick-and-mortar stores.

Most online channels adopt a transparent pricing model of “loose stone + ring setting + low markup,” encouraging consumers to vote with their wallets by choosing the best value for money.

Situation 4: Brands are in disarray

Power Diamond, Mancalon’s Mucan, CRITI RORA under Sifangda, Wald’s Anndia, Shenma’s Pingmei, and various up-and-coming DTC brands… Yet none of them has truly established itself as a “premium cultured diamond brand” in consumers’ minds; most are still locked in a price war centered on “just XXX for a one-carat diamond.”

Traditional jewelry brands (such as China Gold) have just begun to test the waters, but most are adopting a low-risk approach through “partnerships or private labeling.”

Trends: How to Make the Most Critical Leap?

The industry consensus is that the survival of lab-grown diamonds does not hinge on whether they can be made cheaper, but rather on whether they can achieve a shift in perception—from being seen as a “cheap substitute for natural diamonds” to becoming a “standalone category.”

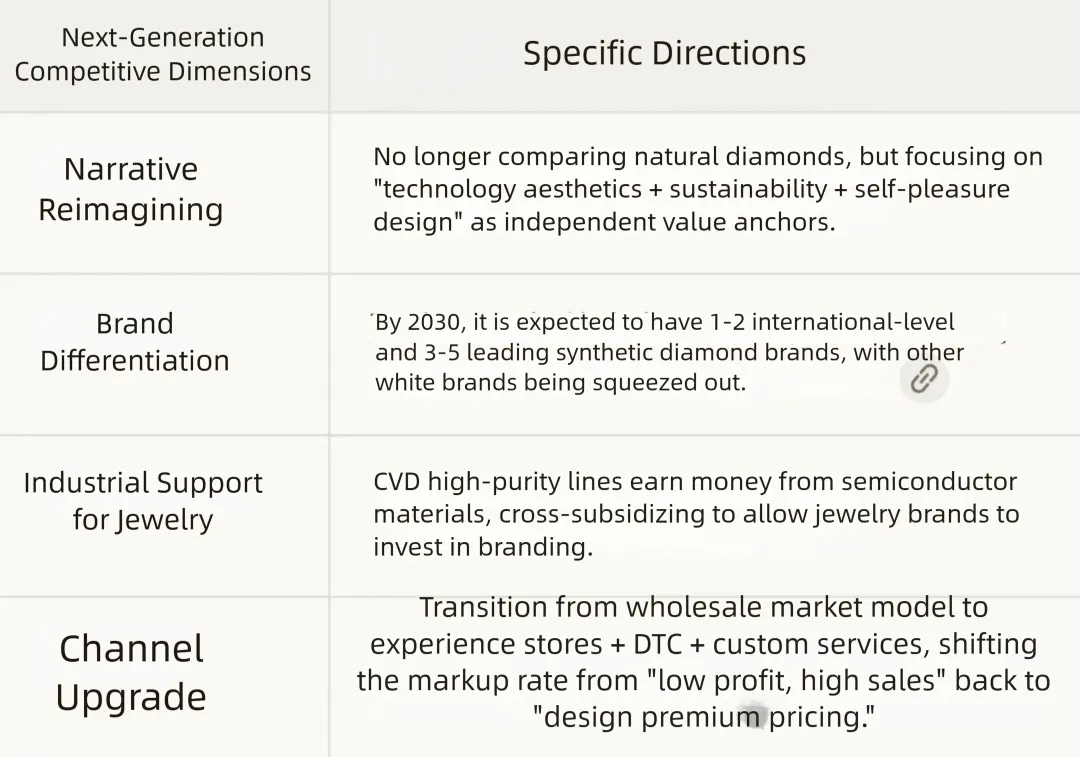

In my view, China’s lab-grown diamond sector requires the development of high-potential brands, much like the new energy vehicle industry, which has evolved from emphasizing value for money to building brand recognition. This involves reshaping brand narratives, differentiating brands, leveraging the upstream industry to support the jewelry sector, upgrading distribution channels, and opening physical stores.

The pain points in the upstream sector are overcapacity and plummeting gross margins → The solution is to clear out inventory in the jewelry segment and develop a second growth curve in the industrial sector (AI cooling/semiconductors);

The midstream’s pain is being locked into low-value-added production in India → The solution is to repatriate high-value-added orders through smart cutting and polishing + gradually build domestic processing capabilities;

The downstream’s pain is having sales volume but no brand, coupled with poor market penetration → The solution is a paradigm shift to establish it as an independent category + design/experience-driven growth rather than pure price wars

To put it simply, lab-grown diamonds are currently in a phase similar to that of electric vehicles between 2012 and 2015—the technology is proven, production capacity has been ramped up, and costs have been driven down. However, whoever can shift the consumer’s mindset from “buy it because it’s cheap” to “buy it because it’s cool/beautiful/worth it” will be the one to reap the juiciest profits in the end.

The most certain winners in this chain are unlikely to emerge from today’s rough diamond price wars, but rather from the two downstream directions of brand development and industrial applications.