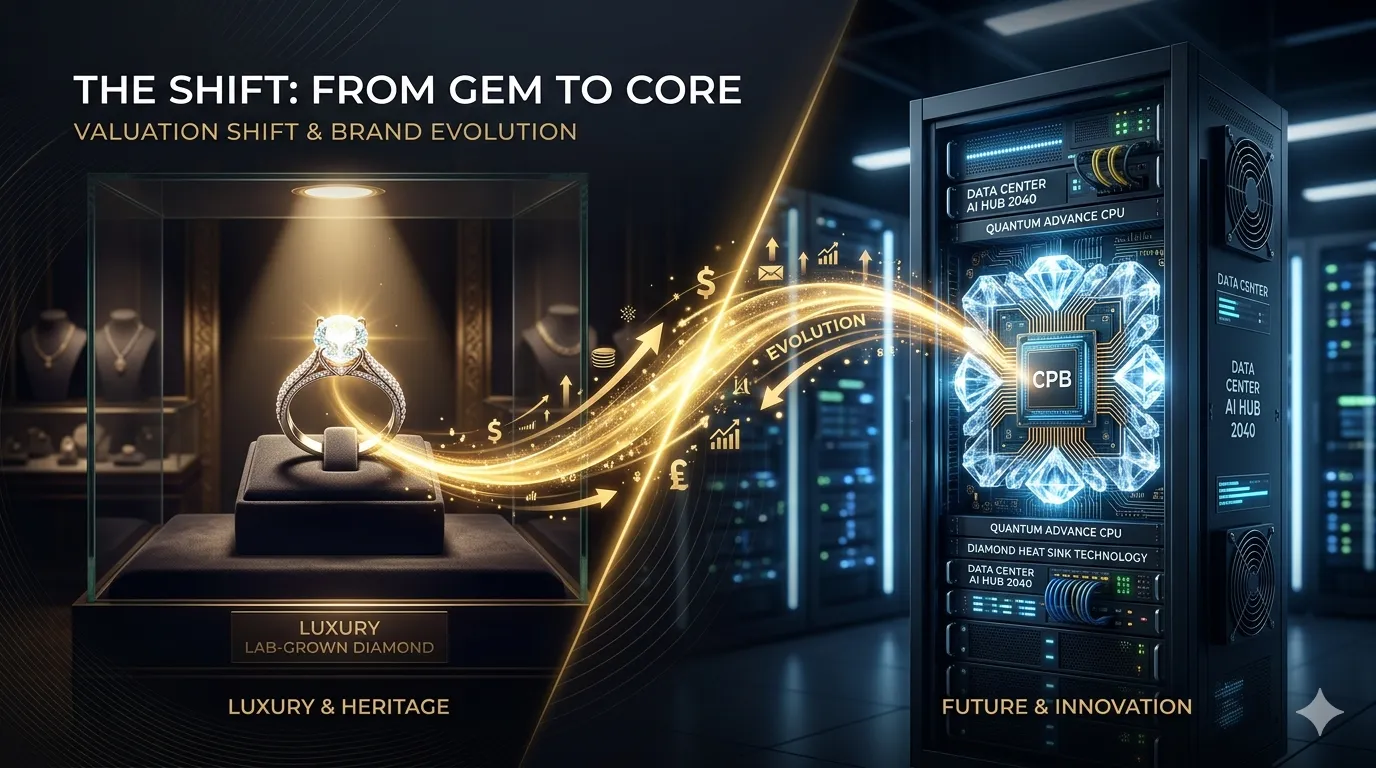

Why Diamond Heat Sink Tech is Redefining Lab-Grown Diamond ROI

The investment thesis for the lab-grown diamond industry has undergone a fundamental “valuation shift” spanning 2025–2026. It is no longer just about “selling shiny jewelry to millennials and Gen Z.” Instead, the sector has unlocked a powerful second growth curve: AI computing cooling and semiconductor thermal management. To evaluate its investment potential, you must first distinguish which curve you are banking on.

Tier 1: Premium Value — The “Advanced Materials” Curve

High-End CVD Diamond → AI & Semiconductor Thermal Management

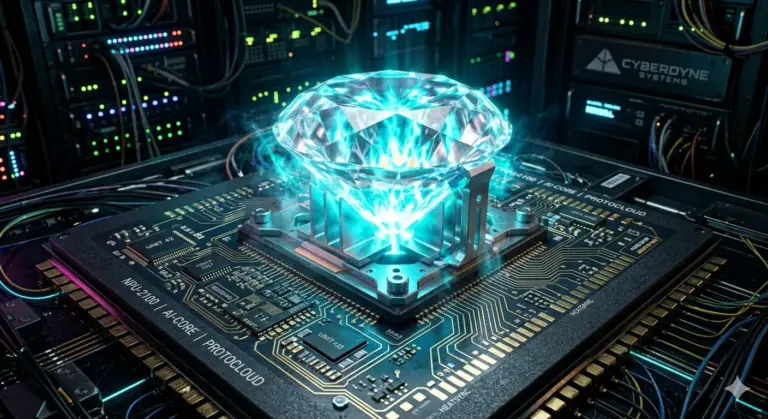

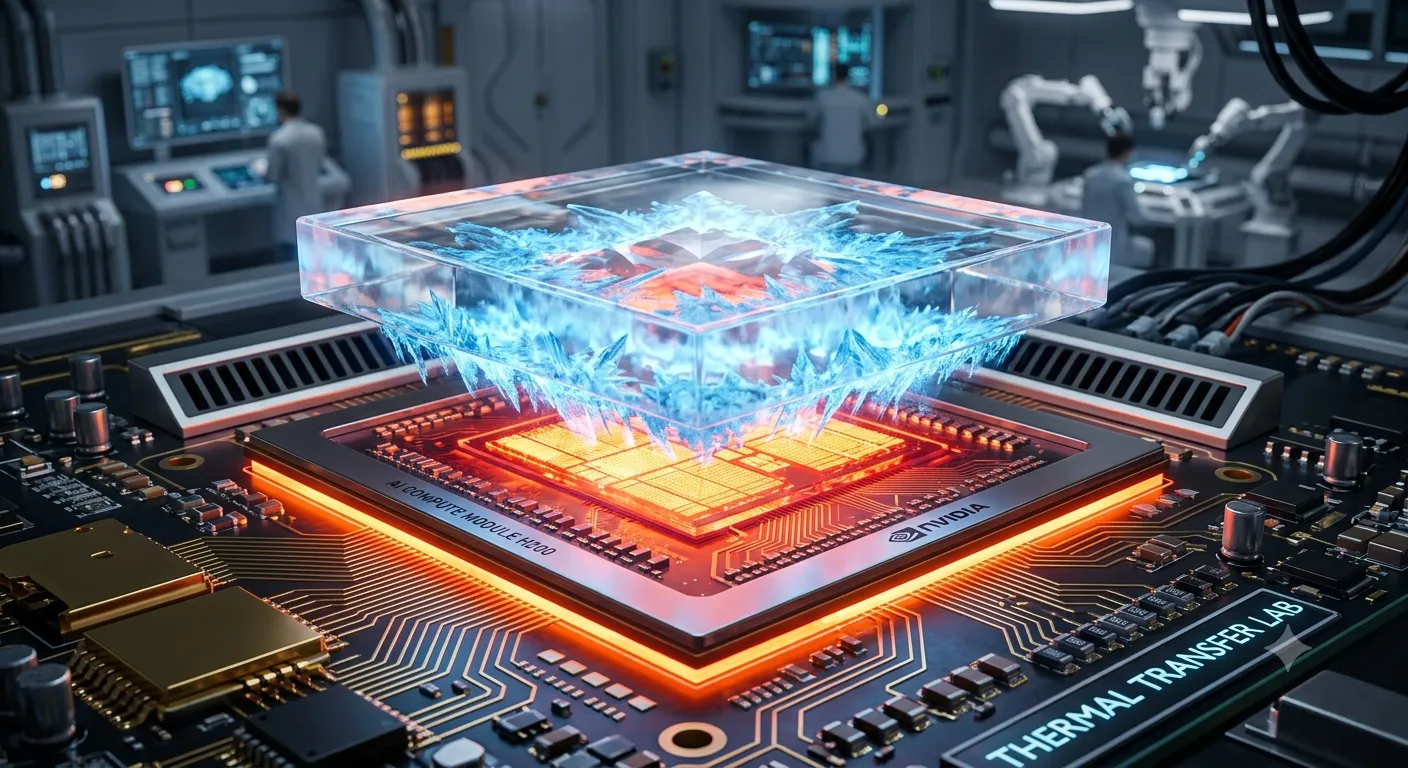

This is where the massive market mispricing lies. The thermal conductivity of diamond is roughly 5.5 times that of copper, positioning the diamond heat sink as the ultimate thermal solution for high-power AI chips like Nvidia’s H200 and AMD’s MI350X.

Not Just Jewelry, But The Ultimate Cooling Material.

- February 2026: The world’s first GPU servers integrated with diamond heat sink components completed commercial delivery.

- May 2026: The Zhengzhou Supercomputing Center scaled up the use of diamond-copper composite materials, boosting heat transfer capability by 80% and successfully entering mainstream data center procurement lists.

- Domestic Production: The first domestic 8-inch diamond heat sink wafer production line launched in Xuchang, Henan, securing early orders from top-tier semiconductor packaging and testing firms.

- Market Forecasts: Guohai Securities projects the global diamond heat sink market to skyrocket from $37 million in 2025 to $15.2 billion by 2030, while Horizon Insights estimates a total addressable market of 48 to 90 billion RMB.

Core Targets (CVD Technical Capacity & Thermal Layout):

- SF Diamond (四方达): Small-batch shipping of GPU diamond heat sink units; 2-million-carat CVD facility capacity.

- Worldia (沃尔德) & Huifeng Diamond (惠丰钻石): Pivoting fiercely toward functional, tech-grade materials.

- Sinomach Precision (国机精工): Controls over 60% of the cubic press market, benefiting directly as a primary hardware supplier.

Risk Note: This segment is in its early “0 to 1” commercialization phase. Expect high growth elasticity matched by high volatility; it trades on tech-material valuations rather than consumer retail metrics.

Upstream Core Equipment — Cubic Presses & CVD Hardware

Whether manufacturing jewelry or a high-performance diamond heat sink, upstream equipment remains the definitive expansion bottleneck.

- Sinomach Precision acts as the crucial “pick-and-shovel seller” for the High-Pressure High-Temperature (HPHT) route. Backed by new national industry standards and strict export controls, its high-end machinery orders show the strongest visibility.

Equipment manufacturers enjoy high entry barriers, clean competitive landscapes, and cash flows that materialize long before the actual diamond producers see returns.

Tier 2: The Cyclical Recovery — Upstream Rough Jewelry Producers

Cost-Fortified Rough Diamond Manufacturers

The brutal price wars of 2022–2024 dragged gross margins from a glittering 70% down to rock bottom. However, a cyclical turning point has arrived:

- By Q4 2025, over 80% of manufacturers issued price increase notices, bumping industrial diamond and rough jewelry diamond prices up by 10% to 15%.

- Heading into 2026, the traditional off-season has remained unseasonably strong, buoyed by a recovery in overseas demand.

s inefficient, small-scale factories face forced liquidation, the surviving titans stand to inherit the market.

Core Targets:

Zhongbing Red Arrow (中兵红箭), SF Diamond (力量钻石), Huanghe Whirlwind (黄河旋风): These players offer a recovery play driven by price stabilization and rising capacity utilization.

The Ceiling: Rough white jewelry diamonds will never return to their historical hyper-profit eras. Treat this tier as a short-term cyclical recovery play, not a buy-and-hold thesis.

Tier 3: High-Status Joint Branding (The “Huawei Automotive” Model)

Investing in brands—whether in the consumer jewelry space or the deep-tech diamond heat sink sector—requires redefining category value. Brand equity acts as a powerful engine for social consensus, but it demands premium storytelling: Who are you? What unique value do you deliver? Where are you heading?

To scale this, companies should look to Huawei’s automotive strategy (the HIMA model: Aito, Luxeed, Stelato). Under a similar framework, an upstream manufacturer partners with downstream giants; the tech pioneer provides the core material breakthrough, capturing steady revenue through technology licensing fees and performance-based sales commissions.

“Not Just Jewelry, But The Ultimate Cooling Material.

Practical Blueprint: Aligning Targets with Your Investment Horizon

Short-to-Medium Term (3–12 Months): Capturing Cyclical Recovery & Tech Catalysts

- Core Thesis: Upstream jewelry de-capacity recovery paired with sudden diamond heat sink speculative catalysts.

- Strategic Allocations:

Equipment Tier: Sinomach Precision (Dominant hardware provider).

Materials Tier: CVD manufacturers with verified diamond heat sink pipelines, specifically SF Diamond and Huifeng Diamond.

Medium-to-Long Term (2–5 Years): Betting on High-Growth Valuation Shifts

- Core Thesis: Mass-scale adoption of diamond heat sinks and semiconductor-grade components.

- The Ultimate Filter: The long-term winners will be the specific companies that secure early validation, testing certification, and recurring purchase orders from global tier-1 semiconductor fabs and consumer electronics giants.

Bottom Line: The Valuation Metamorphosis

The synthetic diamond industry has split cleanly into two distinct ecosystems: traditional consumer luxury and high-margin tech materials.

Whether the growth is fueled by consumer adoption of lab-grown jewelry or the hyper-penetration of the diamond heat sink across tech sectors, Wall Street and global markets will inevitably reward brand equity and proprietary tech over basic factory output.

If you are evaluating this sector purely through the lens of retail jewelry sales, you are missing the boat. The true alpha lies in a simple, disruptive narrative: It is no longer just a luxury ornament; it is the definitive diamond heat sink material for the next generation of computing. The sustainable, long-term premium belongs entirely to proprietary IP and brand value, not raw manufacturing capacity.